All Categories

Featured

Table of Contents

Tax obligation lien investing can give your profile direct exposure to property all without having to in fact have property. Professionals, nonetheless, state the process is made complex and warn that newbie capitalists can easily get burned. Here's whatever you require to understand about spending in a tax obligation lien certification, consisting of how it functions and the dangers included.

The notice normally comes prior to harsher activities, such as a tax obligation levy, where the Internal Revenue Service (INTERNAL REVENUE SERVICE) or local or municipal governments can actually seize someone's residential or commercial property to recoup the financial debt. A tax lien certificate is created when a homeowner has actually stopped working to pay their taxes and the city government concerns a tax lien.

Tax obligation lien certificates are commonly auctioned off to capitalists looking to profit. To recuperate the delinquent tax obligation dollars, districts can then offer the tax lien certification to private capitalists, that care for the tax obligation expense in exchange for the right to collect that money, plus passion, from the homeowner when they at some point repay their equilibrium.

Are Tax Liens Good Investments

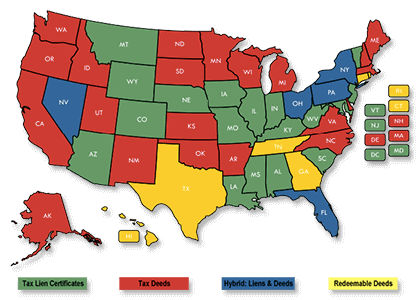

enable the transfer or assignment of delinquent property tax liens to the economic sector, according to the National Tax Lien Organization, a not-for-profit that represents governments, institutional tax obligation lien investors and servicers. Here's what the procedure resembles. Tax obligation lien capitalists have to bid for the certification in an auction, and exactly how that process works relies on the certain district.

Get in touch with tax authorities in your location to make inquiries how those overdue tax obligations are gathered. Public auctions can be on the internet or in person. Sometimes winning bids go to the capitalist happy to pay the lowest rate of interest rate, in a technique known as "bidding down the rate of interest." The municipality establishes an optimum rate, and the prospective buyer supplying the lowest rates of interest under that maximum wins the auction.

Other winning quotes most likely to those that pay the highest possible cash money amount, or costs, above the lien amount. What happens following for financiers isn't something that takes place on a supply exchange. The winning prospective buyer needs to pay the whole tax bill, consisting of the overdue financial debt, interest and charges. The financier has to wait till the residential or commercial property proprietors pay back their entire balance unless they don't.

While some investors can be awarded, others could be captured in the crossfire of complex policies and loopholes, which in the most awful of scenarios can cause substantial losses. From a plain earnings perspective, most investors make their money based upon the tax obligation lien's rate of interest. Interest rates differ and depend on the territory or the state.

Earnings, nevertheless, don't constantly amount to returns that high during the bidding process. In the end, the majority of tax obligation liens bought at auction are sold at prices between 3 percent and 7 percent across the country, according to Brad Westover, executive director of the National Tax Obligation Lien Organization. Prior to retiring, Richard Rampell, formerly the chief exec of Rampell & Rampell, an accountancy company in Hand Beach, Florida, experienced this firsthand.

Tax Lien Real Estate Investing

Then large institutional financiers, including banks, hedge funds and pension plan funds, chased those greater yields in auctions around the country. The larger investors aided bid down passion rates, so Rampell's team had not been making substantial money anymore on liens.

Yet that hardly ever happens: The taxes are generally paid before the redemption day. Liens likewise are very first eligible settlement, even prior to mortgages. Even so, tax obligation liens have an expiration date, and a lienholder's right to seize on the building or to collect their investment ends at the same time as the lien.

Specific capitalists that are taking into consideration financial investments in tax liens should, over all, do their research. Experts recommend staying clear of buildings with ecological damage, such as one where a gas station unloaded hazardous product.

How Does Investing In Tax Liens Work

"You must truly understand what you're acquiring," says Richard Zimmerman, a companion at Berdon LLP, an accounting firm in New York City. "Recognize what the home is, the area and values, so you do not buy a lien that you will not be able to accumulate." Would-be capitalists must additionally take a look at the building and all liens against it, in addition to recent tax obligation sales and price of similar homes.

"People get a listing of residential properties and do their due diligence weeks before a sale," Musa claims. "Fifty percent the homes on the listing may be gone because the tax obligations obtain paid.

Tax Lien Investment Bible

Westover says 80 percent of tax obligation lien certificates are sold to participants of the NTLA, and the firm can frequently compare NTLA participants with the right institutional capitalists. That might make taking care of the process easier, particularly for a newbie. While tax lien financial investments can supply a generous return, understand the fine print, details and rules.

"However it's complicated. You need to recognize the details." Bankrate's contributed to an upgrade of this story.

Real estate tax liens are an investment specific niche that is overlooked by a lot of capitalists. Purchasing tax liens can be a profitable though reasonably dangerous company for those that are well-informed concerning real estate. When people or businesses stop working to pay their real estate tax, the districts or other federal government bodies that are owed those taxes put liens versus the residential properties.

Tax Lien Tax Deed Investing

These insurance claims on security are also exchanged among financiers that want to generate above-average returns. Through this process, the municipality gets its taxes and the capitalist gets the right to collect the amount due plus rate of interest from the debtor. The procedure rarely ends with the investor confiscating possession of the residential or commercial property.

Liens are cost auctions that often involve bidding process battles. If you require to confiscate, there might be other liens versus the building that keep you from occupying. If you get the building, there may be unforeseen expenditures such as repair services or perhaps evicting the current occupants. You can also invest indirectly through building lien funds.

It efficiently locks up the building and stops its sale till the owner pays the tax obligations owed or the building is taken by the creditor. For example, when a landowner or home owner falls short to pay the taxes on their residential or commercial property, the city or area in which the residential property lies has the authority to place a lien on the residential or commercial property.

Property with a lien affixed to it can not be sold or refinanced until the tax obligations are paid and the lien is gotten rid of. When a lien is released, a tax obligation lien certification is developed by the community that shows the quantity owed on the building plus any passion or penalties due.

It's estimated that an extra $328 billion of residential property tax obligations was assessed throughout the U.S. in 2021. It's tough to examine across the country home tax obligation lien numbers.

{kind=link}

Table of Contents

Latest Posts

Find Properties With Tax Liens

Tax Forfeited

Back Tax Homes For Sale

More

Latest Posts

Find Properties With Tax Liens

Tax Forfeited

Back Tax Homes For Sale